Stop the P&L Roller Coaster: Accruals & Inventory

Understanding the True Cost Allocation Behind Your Monthly Financials

In last month’s QuickBooks Tips & Tricks, we looked at two very common improper postings that will cause your P&L to move each month like a roller coaster, and how to fix them. They are the most common cause, but the amounts they affect are normally much less than the two we will be looking at this month.

I can’t stress enough about the importance of “Closing Your Books” each month properly. Often, this one lack of process can wreak havoc on the accuracy of your financial statements.

Remember, it is a key point to always analyze your business on an Accrual Basis. Accrual Basis analysis allows for the expenses to be taken in the month they occurred, and not necessarily when they were paid. This is a key feature for creating a “Bill” in the month the expense was due, as shown in last month’s information.

This Month’s Focuses:

Other Accruals

Inventory Adjustments (Or actually the lack of them each month)

Other Accruals

Accruals, or the lack of them, can cause specific months to fluctuate, and many business owners don’t consider how much they affect monthly financials. So what are Accruals? They are expenses to your business similar to the Pre-Payments we looked at in our last month’s tips, but almost in reverse.

Expenses That Should Be Accrued Regularly:

Vacation Pay

Sick Days / Paid Time Off (PTO)

Holidays

Year-End / Quarterly Bonuses

IRA Employer Contributions

401K Employer Match Contributions

As an example: Year-End Bonuses. Was the bonus actually just for December? Or was it a bonus for the services performed for the entire time they worked during that year? These expenses, when improperly posted, hit the financials for only one month when they should have been accruing and spread over a longer period.

At the beginning of each year, you should determine your yearly “Budget” for your accruing expenses and divide it by the number of months it represents. Then, create a memorized transaction (either a Journal Entry or a Zero-Dollar Check) to add it to the Accrual Account and cost it to the appropriate Expense Account monthly.

Figure 1 – Memorized Accrual Entry Example

When the payment is actually made, it is charged against the Accrual Account, not the expense account. This way the actual costs are distributed for the entire time they represented, and not all at once during a specific month. This can have a significant impact on specific months, especially December.

Figure 2 – Charging Payments to the Accrual Account

Even month-end or quarterly bonuses should be accrued before the month is closed, so they can be paid accordingly in the following months.

Inventory Adjustment

In many businesses, there is a large amount of inventory present to expedite processing. In service businesses, this is often a major reason why the P&L moves so much each month if not accounted for properly.

It may be a wise decision to purchase fast-moving products in larger quantities to get better pricing, but it does not mean the cost of these purchases should hit the P&L all at once either.

💡 The Golden Consumption Rule

It is not correct to “cost out” the purchases for products used in your business unless they are actually consumed during that accounting period. In other words, just because you bought it and paid for it doesn’t mean you should cost it out 100% unless it is fully consumed during that same month. This is the point of tracking and managing inventory.

QuickBooks does have a rudimentary inventory program built into QuickBooks Pro and Premier, and a more advanced program available in Enterprise. However, for most service businesses, this program isn’t quite what is needed.

In service-type businesses, there are many third-party options that allow you to track and manage your inventory. Setting them up does take a little time and planning, but it is well worth it. Many of these third-party systems are included with your vendor relationships or as part of an industry management system. They often feature barcode scanning, job cost allocations, and invoicing capabilities.

What Should Be Considered Inventory?

Office & Admin Supplies

Boxes of Copy Paper

Laser/Inkjet Cartridges

Blank Checks & Stationery

Cleaning & Maintenance Supplies

Operational Stock (e.g., Shop/Auto)

Antifreeze, Oils, and Filters

Tires, Bulbs, and Fuses

Nuts, Bolts, and Clips Assortments

Refinish Paints, Clears, and Toners

Depending on your business, you may be tracking costs for inventory in several General Ledger Accounts (GL). Cost Accounts may include Cost of Goods Sold (COGS) for Parts, Materials, and Supplies, or other supply/safety items being tracked as an Expense.

Month End Inventory Adjustments

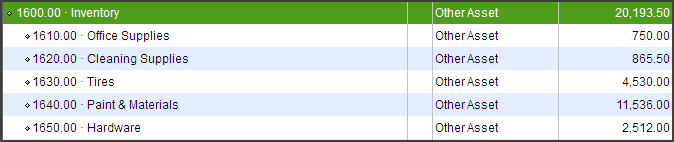

Setting up an inventory control system with categories for different types of inventory is important, since the monthly adjustment may need to be performed on different GL accounts. Having different categories set up makes it easy to distribute the adjustment to those different accounts.

Figure 3 – Typical Inventory Accounts Breakdown

There are two basic methods to handle inventory each month. Both require a way to evaluate your inventory value each month. A physical inventory count (conducted quarterly or at year-end) will also be needed to verify system values and identify areas of possible theft.

Method 1: Adjusting by Inventory Value Change

During the month, all vendor invoices (Bills) for items purchased for inventory are coded and distributed to their normal COGS or expense accounts. At the end of the month, the net “Change to Your Inventory Value” is used to adjust your COGS and Expense Accounts.

Figure 4 – Inventory Adjustment Journal Entry (Method 1)

Figure 5 – Asset Account Adjustments (Method 1)

Method 2: Allocating Purchases to Inventory Asset First

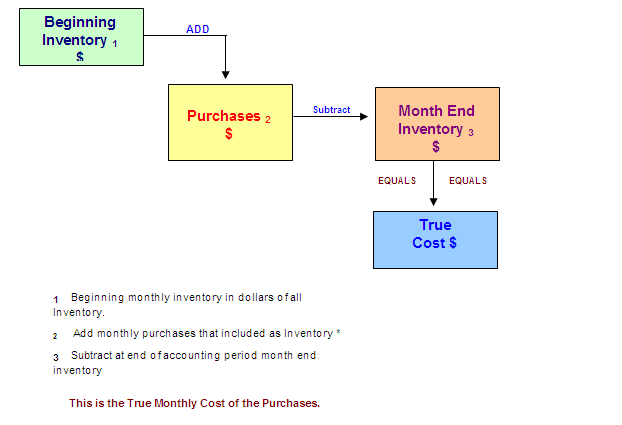

The second method requires that all Vendor Invoices (Bills) for inventoried items purchased during the month are distributed to an Inventory Asset Account instead of a COGS or expense account. Then, at the end of the month, the true cost of your consumed purchases is calculated and adjusted from Inventory into your COGS or expense accounts.

📐 How to Determine Your True Monthly Cost:

Practical Example:

Your tire inventory at the beginning of the month was $17,500.00. During the month, your purchases totaled $10,000.00. Your ending inventory value was evaluated at $16,500.00.

$$\text{True Cost Month End Tire COGS} = \$17,500.00 + \$10,000.00 – \$16,500.00 = \$11,000.00$$

Figure 7 – Entering the True Cost Adjustment (Method 2)

Evaluating inventory value at the end of each month is the key to properly managing your assets and determining the adjustments needed to properly account for fluctuations. From examining hundreds of financial records for small businesses worldwide, this is the second leading cause for roller-coaster financials, but it is almost never accounted for properly. Isn’t it time to begin managing your Inventory?

In next month’s issue, we will conclude our look at what normally is the single greatest cause of roller-coaster P&Ls: Work in Process (WIP).

Planning for Year End

We have just finished our Labor Day Holiday, and we are going to finish up the third calendar quarter before you know it. This is the time to begin planning for year-end and the new year as well—not in November or December.

Is your company file getting too large? Are you getting close to the limits we have discussed in previous issues? This is the time to assess the situation and make plans. Waiting until your company file crashes can cost you a lot of frustration and extra money.

Are you thinking about upgrading your Chart of Accounts to reflect better details for your financials? If so, the best transition window is at year-end. To schedule this type of project, it needs to be set up now.

Closing your QuickBooks at the end of the year needs to be a high priority. Doing the year-end closing normally requires a great deal of “Clean Up” to correct accounts and verify them for a successful new year start before handing them over to your CPA for tax preparation.

💬 Tell Us What You Think!

We are constantly refining our content to better serve Collision Repair shops and small businesses worldwide. Please take 2 minutes to fill out our quick survey and tell us what topics you would like to see us cover in the future!

Need Help Reconciling or Setting Up Your Systems?

Our company AEII, QuickBooks R Us, is here to assist small businesses with clean-up services, training, and custom setup options. Let us help you align your systems so you can make informed decisions.

📅 Book a Reconcile Session

Free 30-Min Consultation • No Obligation

If you have missed our earlier issues of QuickBooks Tips & Tricks, you can catch up on past issues by Clicking Here.

Thank You, and I look forward to sharing more QuickBooks Tips and Tricks with you next month …